Original Medicare — which is Medicare Part A and Part B combined — helps to cover many healthcare costs. But even with Medicare, you’ll still be responsible for some expenses like copayments and deductibles, which can fees can quickly add up.

A Medigap policy, also called a Medicare Supplement plan, can help to cover these out-of-pocket costs so the expenses you’re responsible for are minimized or eliminated. Your Original Medicare first contributes toward its share of your healthcare expenses. Then, your Medigap policy will help to cover some or all of the remaining fees.

What You Need to Know

Original Medicare covers many of your healthcare expenses, but you’ll still be responsible for some costs like copayments and deductibles. A Medigap plan can help to cover these fees.

You must be enrolled in Medicare Parts A and B to qualify for a Medigap policy.

In Utah, you can choose from 12 Medigap plans, including two high-deductible options.

When Can You Enroll in Medigap?

It is easiest to enroll in Medigap during your six-month Open Enrollment Period.1 Your Open Enrollment Period automatically starts the month that you turn 65 and are enrolled in Medicare Part B. During this period, you can buy any plan, even if you have a preexisting health condition like diabetes. If you need to make changes to your policy, you can do so during this time.

You can still enroll in Medigap outside of Open Enrollment, but the process becomes more complicated. After your Open Enrollment Period ends, insurance providers can increase the cost of your plan or deny you coverage for a preexisting condition. The provider might require a six-month waiting period before your coverage takes effect, and your coverage might exclude any preexisting condition you may have.

However, there are a few situations where you can still enroll in Medigap outside of Open Enrollment without these restrictions. You might qualify for guaranteed issue rights because of certain events like moving outside of your Medicare Advantage Plan’s service area.2 When you have guaranteed issue rights, an insurance provider is required to let you buy a Medigap policy without implementing a waiting period, excluding a preexisting condition, or increasing your policy cost. The situations that qualify you for guaranteed issue rights are very specific, so review the restrictions closely.

You might also qualify for a Special Enrollment Period, which allows you to make changes to your coverage.3 Qualifying events include losing your current coverage or moving. The types of changes you can make to your policy will depend on the type of event that qualified you for a Special Enrollment Period.

A Word of Advice

It’s best to enroll in a Medigap policy during your initial Open Enrollment window right after you turn 65. You’ll have the most flexibility in buying or changing plans during this time.

What Are the Most Popular Medicare Supplement Plans?

| Plan Type | Total Enrolled (Rounded) | Percent of Total Enrolled |

| Plan F | 48,000 | 56% |

| Plan G | 22,000 | 26% |

| Plan N | 9,000 | 10% |

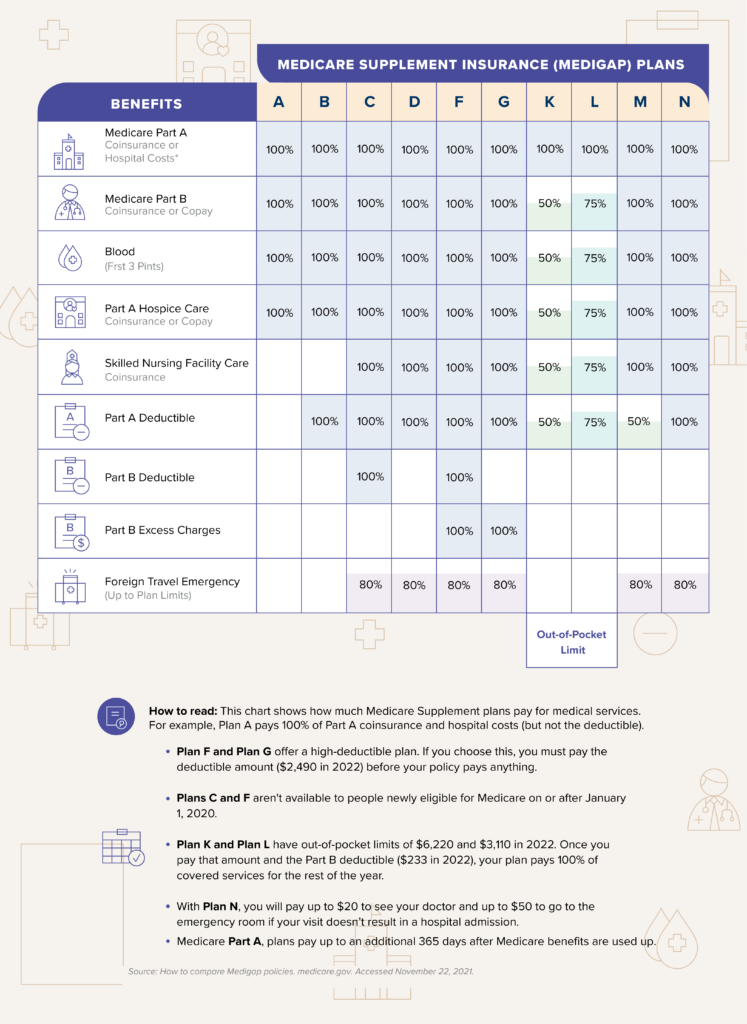

In Utah, you can choose from 12 Medicare supplement plans, including two high-deductible options.4 Coverage, premiums, deductibles, and copayments can vary, so review each policy carefully to understand just what’s included. Plans F, G, and N are some of the most popular options. Note: Plans C and F are not available to anyone who qualified for Medicare after January 1, 2020.

Plan F

Plan F is the most comprehensive option, which covers:

- Part A coinsurance and hospital costs

- Part B copays/coinsurance

- Blood (first 3 pints)

- Part A hospice

- Skilled nursing facility

- Part A deductible

- Part B deductible

- Part B excess charges

- Foreign travel emergency – 80%

Plan G

Plan G offers similar coverage as Plan F, but it excludes coverage for the Part B deductible:

- Part A coinsurance and hospital costs

- Part B copays/coinsurance

- Blood (first 3 pints)

- Part A hospice

- Skilled nursing facility

- Part A deductible

- Part B excess charges

- Foreign travel emergency – 80%

Plan N

Plan N offers coverage that’s similar to Plan G, but it excludes the Part B deductible and Part B excess charges:

- Part A coinsurance and hospital costs

- Part B copays/coinsurance

- Blood (first 3 pints)

- Part A hospice

- Skilled nursing facility

- Part A deductible

- Foreign travel emergency – 80%

How to Choose a Medicare Supplement Plan

Each Medigap plan offers different coverage, so depending on the types of healthcare costs that you most frequently incur, certain plans may be better fits than others. If you choose a plan that covers your most common expenses, you may get better value than choosing a plan with a lower premium that you don’t end up using often. When comparing the different policies, look for a plan that strikes a balance of good coverage with a premium that you can comfortably afford.

Good to Know

The cost of Medigap policies can vary widely. Rather than simply going for the cheapest plan, be sure to consider what each option includes and what level of coverage would benefit you the most.

How Much Do Medigap Policies Cost?

The cost and coverage of Medigap policies varies depending on the plan. Copayments and deductibles can also differ. The following fees are for a 65-year-old female and male in Utah who doesn’t use tobacco. These estimates can give you a rough idea of plan premiums:

65-Year-Old Woman, No Tobacco Use

| Plan Type | Premium Range |

| Plan F | $106-$367 |

| Plan G | $97-$351 |

| Plan N | $68-$265 |

65-Year-Old Man, No Tobacco Use

| Plan Type | Premium Range |

| Plan F | $118-$414 |

| Plan G | $106-$397 |

| Plan N | $76-$299 |

What Companies Sell Medigap in Utah?

What If You Want to Change Your Medigap Policy?

As discussed earlier, you can easily change your Medigap policy during your Open Enrollment Period. Once Open Enrollment has ended, there are only a few situations where you can change your plan.5 With a Special Enrollment Period or guaranteed issue rights, you will be able to change your policy, but the types of changes that you can make may be limited. Rather than relying on one of these situations, it’s best to thoroughly research all of the plans before enrolling in one. By choosing the best plan for your needs during your Open Enrollment Period, you won’t have to worry about changing it later.

What Are Alternatives to Medicare Supplement?

Medigap policies aren’t right for everyone. If you’re interested in additional coverage, you might also consider a Medicare Advantage plan. Like Medigap policies, Medicare Advantage plans help to cover the remaining Medicare Part A and Part B expenses that you’re responsible for.6 While Medigap plans don’t offer prescription coverage, some Medicare Advantage plans do help to cover drug costs.

What Are Medicare Resources in Utah?

- The Utah State Health Insurance Assistance Program (SHIP) provides free one-on-one counseling to help you choose and enroll in the Medicare plan that’s right for your needs. You can reach this program at 1-800-541-7735.

- The Utah Insurance Department provides resources that can help you to understand and shop for insurance. You can also file a complaint against an insurance company or agent through this department.

- You can enroll in Medicaid online through the Utah Department of Health Medicaid, and its Health Program Representatives can help you to learn about your Medicaid benefits and options.

Snippet Render Is Present – D3 cannot be loaded in editor mode. Go to preview or publish mode.

Next Steps

While Medicare covers many healthcare expenses, the costs that you’re responsible for — like copayments and deductibles — can quickly add up. Enrolling in a Medigap plan may help to reduce or even eliminate your out-of-pocket fees. To learn more, check out How to Choose a Medicare Supplement Plan.