Written by Melinda Sineriz

HealthCare Writer

We aim to help you make informed healthcare decisions. While this post may contain links to lead generation forms, this won’t influence our writing. We follow strict editorial standards to give you the most accurate and unbiased information.

What You Need to Know

- Medicare Supplement plans, also known as Medigap, help pay for out-of-pocket costs not covered by Medicare Part A and Part B.

- Montana insurance companies must accept your Medicare Supplement (Medigap) plan application if you’re in your Medigap Open Enrollment Period or have guaranteed issue rights.

- The three most popular Medigap policies are typically Plans F, G, and N.

What Are Medicare Supplement Plans in Montana?

Medicare is a federal health insurance program for individuals aged 65 and older, as well as younger people with qualifying disabilities or health conditions (e.g., end-stage renal disease).

Original Medicare includes Part A (Hospital Insurance) and Part B (Medical Insurance), which cover many healthcare services. However, out-of-pocket costs like deductibles, coinsurance, and copayments can still apply. Medicare Supplement plans help pay for these expenses.

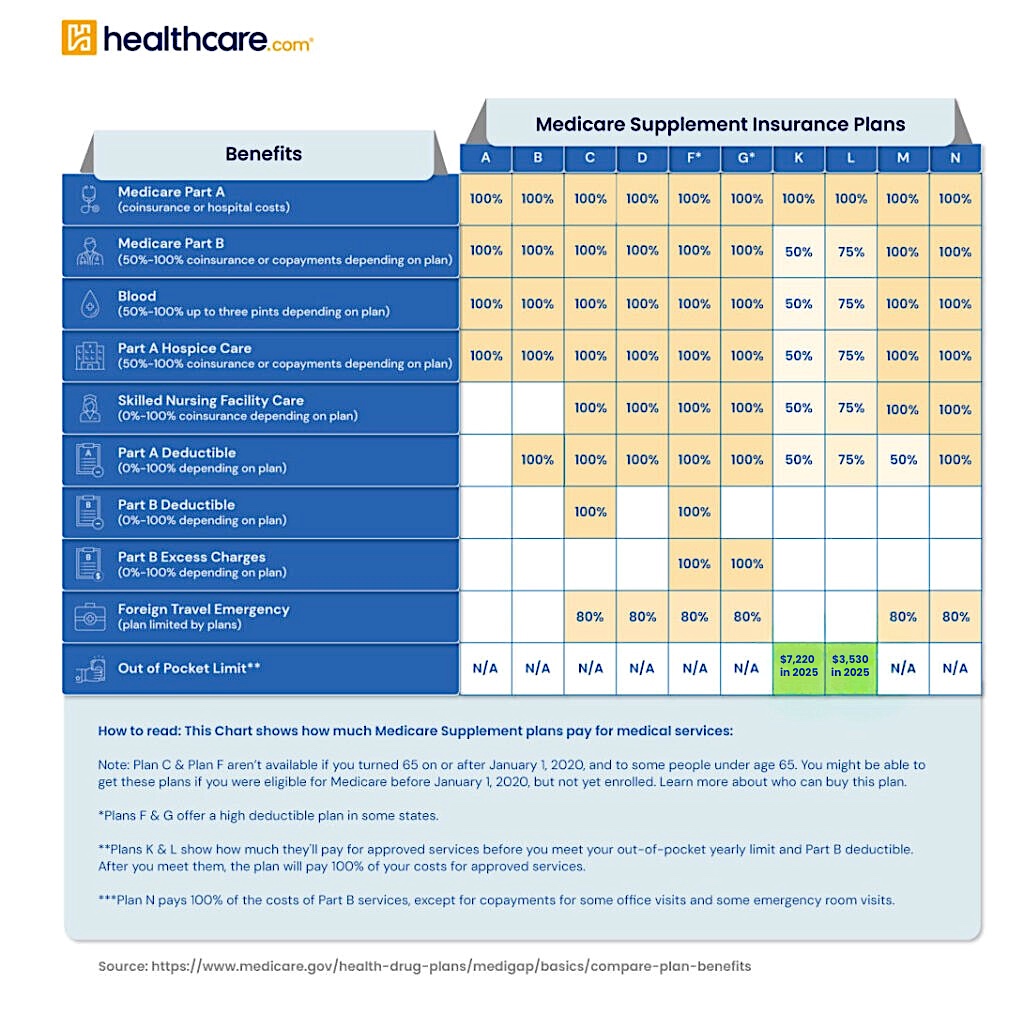

Medigap plans are standardized by letter (A through N), which means Plan G from one insurer offers the same coverage as Plan G from another. The only difference is typically the premium charged.

Learn how these plans work and how they benefit residents of Montana.

Compare options HERE & start your health plan journey.

When Can You Enroll in a Medicare Supplement (Medigap) Policy?

You can apply for a Medigap plan at any time. However, outside of your Medigap Open Enrollment Period—or without guaranteed issue rights—insurers may decline your application or charge more based on your health history.

Your Open Enrollment Period lasts six months and begins when you’re both age 65 or older and enrolled in Medicare Part B. During this window, insurance companies must accept your application regardless of any preexisting conditions.

Guaranteed issue rights allow you to enroll in a Medigap plan outside your Open Enrollment Period without being penalized for your health status. These rights may apply if:

- You leave a Medicare Advantage plan within the first year

- Your Medicare Advantage plan exits Medicare or you move out of its service area

- You lose group coverage from an employer or union

- Your Medigap insurer goes bankrupt

- You were misled by your insurance provider

In these cases, insurers cannot deny your application or charge you more based on your medical history.

What Are the Most Popular Medicare Supplement Plans?

Nationwide, the most common Medigap plans include:

- Plan F – Offers the most comprehensive benefits but is only available to those who became eligible for Medicare before January 1, 2020.

- Plan G – Covers everything Plan F does except the Medicare Part B deductible. It is the most popular plan for new Medicare enrollees.

- Plan N – Offers a lower-cost alternative with copayments for some services. It doesn’t cover the Part B deductible or excess charges.

These plans are widely available in Montana and provide robust coverage for beneficiaries looking to reduce out-of-pocket expenses.

How Do You Choose a Medicare Supplement Plan?

To select the best Medigap plan in Montana:

- Decide which plan letter (such as G or N) meets your needs.

- Use tools like the Medicare Plan Finder or speak with a licensed insurance agent to identify which insurers offer these plans in your area.

- Understand that while plan benefits are standardized, premium prices can vary by insurer.

Insurers in Montana may use different pricing methods:

- Community-rated – Premiums are the same for all enrollees.

- Issue-age-rated – Premiums are based on your age at the time of enrollment and do not increase with age.

- Attained-age-rated – Premiums are based on your current age and may increase as you get older.

Always compare the same lettered plan across different insurers to find the best value for your situation.

How Much Do Medigap Policies Cost?

Medigap premiums in Montana vary based on:

- Age and gender

- Tobacco use

- Chosen plan type (e.g., Plan G or Plan N)

- Pricing method used by the insurer

Although coverage remains the same for a specific plan letter, monthly premiums can vary significantly depending on the provider and pricing structure.

Compare options HERE & start your health plan journey.

What If You Want to Change Your Medicare Supplement Plan?

You can apply to switch your Medigap plan at any time. However, unless you qualify for guaranteed issue rights, the insurer may evaluate your medical history and either deny coverage or charge higher premiums based on your health.

If you’re approved for a new policy, remember to cancel your previous Medigap plan so you aren’t paying for duplicate coverage.

What Are Alternatives to Medicare Supplement Plans?

Medicare Advantage plans, also known as Part C, are offered by private insurance companies approved by Medicare. These plans bundle Part A and Part B, and most include Part D prescription drug coverage.

Many Medicare Advantage plans also offer extra benefits such as routine dental, vision, hearing, and fitness programs.

If you prefer a single policy that combines medical, hospital, and drug coverage, Medicare Advantage may be a suitable alternative.

Learn more about Montana Medicare Advantage plans.

Medicare Part D

Medicare Part D plans provide standalone prescription drug coverage.

- Who needs it: If you have Original Medicare (Part A and/or Part B) and want drug coverage

- What it covers: Prescription medications, with plan specifics varying by provider

- How it’s offered: Through Medicare-approved private insurance companies

- Not needed if: You are enrolled in a Medicare Advantage plan that includes prescription coverage (MAPD)

Shop for a Medicare plan with additional benefits!

Do Medigap Plans Cover Prescription Drugs?

No. Medicare Supplement plans do not cover prescription medications. If you need prescription coverage, you’ll need to enroll in a separate Medicare Part D plan.

Medicare Resources in Montana

Montana residents can access free help and support through these resources:

- State Health Insurance Assistance Program (SHIP) – Provides one-on-one Medicare counseling. Call 1-800-551-3191.

- Montana Commissioner of Securities and Insurance – Handles complaints related to Medicare insurance. Contact 1-800-332-6148.

- Montana Medicaid (Office of Public Assistance) – Offers coverage for low-income individuals and may work with Medicare. Apply online or call 1-888-706-1535.

Next Steps

If a Medicare Supplement plan in Montana fits your healthcare and financial needs, consider comparing plans and enrolling during your Medigap Open Enrollment Period.

Use online tools or reach out to a licensed insurance agent to explore your options and receive personalized guidance.

Thank you for your feedback!

U.S. Government Website for Medicare. “Choosing a Medigap Policy: A Guide to Health Insurance for People With Medicare.” medicare.gov (accessed February 19, 2021), 9.

“Choosing a Medigap Policy: A Guide to Health Insurance for People With Medicare.” 14.

“Choosing a Medigap Policy: A Guide to Health Insurance for People With Medicare.” 21-23.

America’s Health Insurance Plans. “State of Medigap: Trends in Enrollment and Demographics.” ahip.org (accessed February 19, 2021), 7.

“Choosing a Medigap Policy: A Guide to Health Insurance for People With Medicare.” 11.

“Choosing a Medigap Policy: A Guide to Health Insurance for People With Medicare.” 17-18.

“Choosing a Medigap Policy: A Guide to Health Insurance for People With Medicare.” 12.

“Choosing a Medigap Policy: A Guide to Health Insurance for People With Medicare.” 50.

“Choosing a Medigap Policy: A Guide to Health Insurance for People With Medicare.” 17-18.