Written by Howard Yeh

Co-Founder & Chief Revenue Officer at HealthCare.com

Compare Medicare Advantage and Medigap Plans That Fit Your Needs

You will be taken to

to finish your submission.

What You Need to Know

- Medicare Supplement plans, also known as Medigap, help pay for out-of-pocket costs not covered by Medicare Part A and Part B.

- District of Columbia insurance companies must accept your Medicare Supplement (Medigap) plan application if you’re in your Medigap Open Enrollment Period or have guaranteed issue rights.

- The three most popular Medigap policies are typically Plans F, G, and N.

What Are Medicare Supplement Plans in the District of Columbia?

Medicare is a federal health insurance program for individuals aged 65 and older, as well as younger people with qualifying disabilities or health conditions (e.g., end-stage renal disease).

Original Medicare, which includes Part A (Hospital Insurance) and Part B (Medical Insurance), covers many healthcare services. However, it still leaves you with out-of-pocket costs like deductibles, coinsurance, and copayments. Medicare Supplement plans help pay for these expenses.

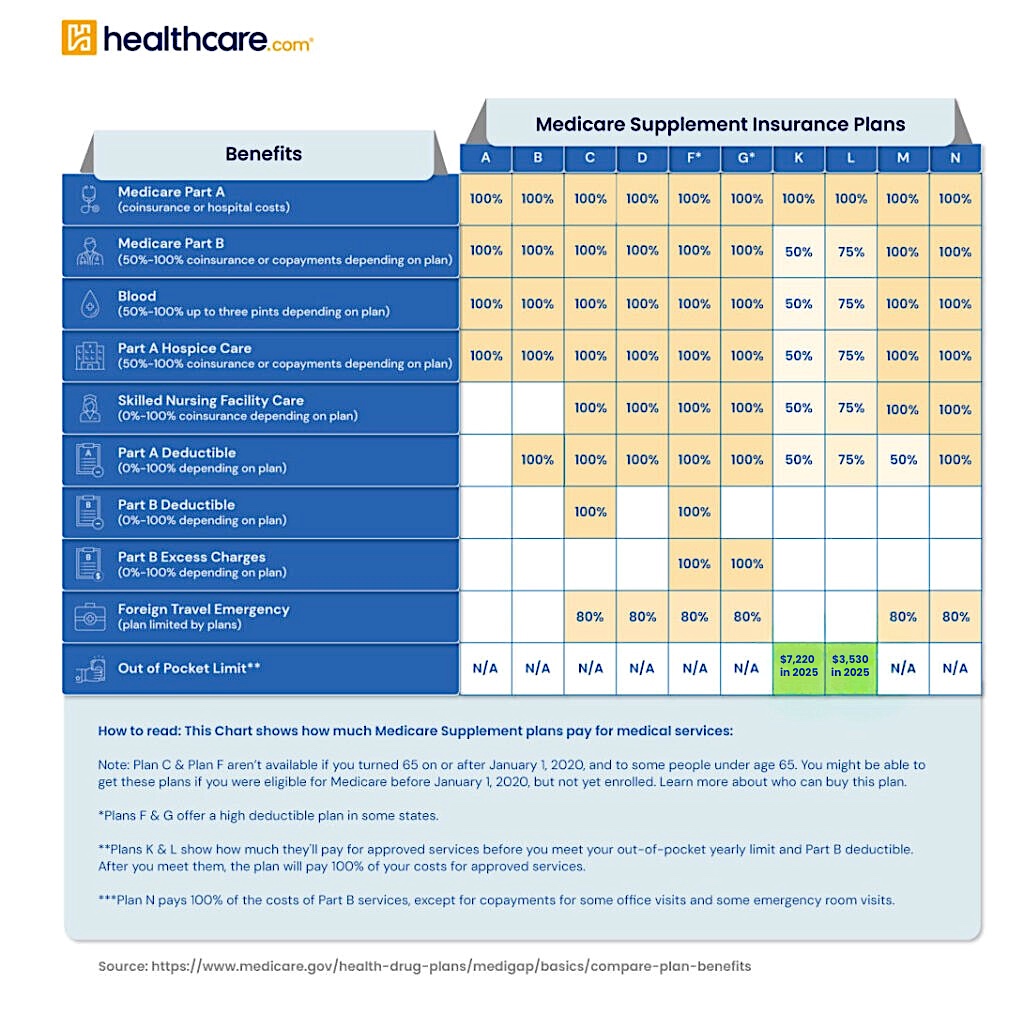

Medigap plans are standardized by letter (A through N). This means that Plan A from one company offers the same benefits as Plan A from another, though premiums and customer service may vary.

Learn how these plans work and how they benefit residents of the District of Columbia.

Compare options HERE & start your health plan journey.

When Can You Enroll in a Medicare Supplement (Medigap) Policy?

You can apply for a Medigap plan at any time. However, outside of your Medigap Open Enrollment Period—or without guaranteed issue rights—insurers may review your health history to determine eligibility and pricing.

Your Medigap Open Enrollment Period lasts six months. It begins when you are both 65 or older and enrolled in Medicare Part B. During this time, insurance companies must offer you any plan they sell at standard rates, regardless of your health.

Guaranteed issue rights may apply if:

- You move out of your Medicare Advantage plan’s service area.

- Your employer health plan or Medigap policy ends.

- You leave a Medicare Advantage plan within the first year and return to Original Medicare.

- Your Medigap insurer misled you or went bankrupt.

If you’re under 65 and on Medicare due to disability or ESRD, availability of Medigap plans may be limited until you reach 65.

What Are the Most Popular Medicare Supplement Plans?

Nationwide and in D.C., the most commonly selected Medigap plans are:

- Plan F – Offers the most comprehensive coverage, but is only available to individuals who became eligible for Medicare before January 1, 2020.

- Plan G – Covers nearly all costs except the Medicare Part B deductible.

- Plan N – Covers most major costs but requires copayments for some doctor and ER visits and does not cover Part B excess charges.

These three plans offer varying levels of coverage and cost-sharing, allowing beneficiaries to choose one that aligns with their healthcare usage and budget.

How Do You Choose a Medicare Supplement Plan?

To choose the right Medigap plan in the District of Columbia:

- Select a plan letter (e.g., G or N) that meets your needs based on how often you use healthcare services and your expected costs.

- Compare insurers that offer your chosen plan. While the coverage is the same, pricing and service vary.

- Understand pricing methods used by insurers:

- Attained age rating: Premiums increase as you age.

- Issue age rating: Premiums are based on your age at the time of purchase.

- Community rating: Everyone pays the same rate, regardless of age.

It’s essential to compare “apples to apples”—Plan G from one insurer versus Plan G from another.

How Much Do Medigap Policies Cost?

Medigap premiums in the District of Columbia vary based on several factors:

- Your age and gender

- Tobacco use

- Plan type

- The insurer’s pricing model

Though plan benefits are standardized, premiums and pricing methods differ. Always request quotes from multiple insurers.

Compare options HERE & start your health plan journey.

What If You Want to Change Your Medicare Supplement Plan?

You can apply to change your Medigap policy at any time. However, unless you qualify for guaranteed issue rights, insurers may use medical underwriting to decide whether to accept your application or adjust pricing based on your health status.

What Are Alternatives to Medicare Supplement Plan?

Medicare Advantage plans, also known as Part C, are a bundled alternative to Original Medicare. These plans are offered by private insurance companies and include:

- Part A (hospital insurance)

- Part B (medical insurance)

- Most plans also include Part D (prescription drug coverage)

In addition, many Medicare Advantage plans offer extras like dental, vision, hearing, and wellness programs. Instead of having separate Medigap and Part D coverage, you might prefer an all-in-one Medicare Advantage plan.

Learn more about District of Columbia Medicare Advantage plans.

Medicare Part D?

Medicare Part D plans provide standalone prescription drug coverage.

- Who needs it: Those with Original Medicare (Part A and/or Part B) who want drug coverage.

- What it covers: Prescription medications. Coverage varies by plan.

- How it’s offered: Through private Medicare-approved insurers.

- Not needed if: You are enrolled in a Medicare Advantage plan with prescription coverage (MAPD).

Shop for a Medicare plan with additional benefits!

Do Medigap Plans Cover Prescription Drugs?

No. Medigap plans do not cover prescription drugs. You must enroll in a separate Medicare Part D plan to receive medication coverage.

Medicare Resources in the District of Columbia

Residents of Washington, D.C., can access several free resources for Medicare support:

- State Health Insurance Assistance Program (SHIP): Provides counseling, assistance with Medicare Supplement plans, and help resolving medical billing issues.

- Department of Insurance, Securities and Banking: Manages Medigap complaints and consumer protections.

- District Medicaid Program: Offers low-cost or free healthcare coverage for individuals with limited income and may work alongside Medicare.

Next Steps

If a Medicare Supplement plan in the District of Columbia suits your needs, begin by choosing the plan letter that fits your health and financial situation.

Compare offerings from multiple insurers and confirm how they set premiums.

For drug coverage, consider enrolling in a separate Part D plan or explore all-in-one Medicare Advantage options.

We aim to help you make informed healthcare decisions. While this post may contain links to lead generation forms, this won’t influence our writing. We follow strict editorial standards to give you the most accurate and unbiased information.

U.S. Government Website for Medicare. “Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare.” medicare.gov. Accessed March 30, 2021. 9.

“Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare.” 14.

“Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare.” 23.

“Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare.” 15.

“Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare.” 49.

America’s Health Insurance Plans. “State of Medigap: Trends in Enrollment and Demographics.” ahip.org. Accessed March 30, 2021. 8.

“Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare.” 11.

“Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare.” 18.

“Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare.” 7.

“Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare.” 50.