A Government Report Projects Long-Term Care Needs Through 2065

America’s population is aging. By 2065, the Social Security Administration projects 95 million people will be 65 and up.

With the growing number of elderly will come growing numbers of people with disabilities. In 2065, 15% of Americans age 65+ will live with at least two disabilities.*

As a result, the number of people using long-term care services for help with activities like bathing and eating will double from 7 to over 14 million Americans in 2065.

Dramatic Rise Seen in Need for Long-Term Care

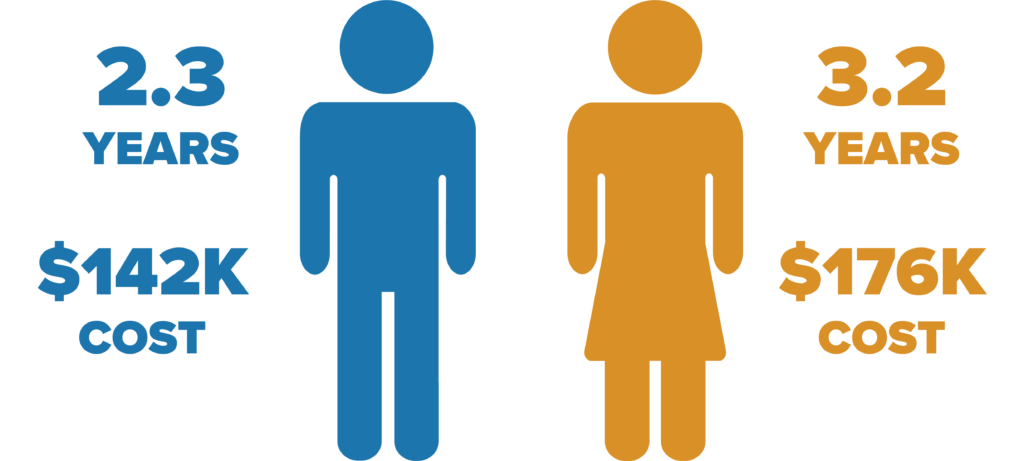

American men who turn 65 in the next few years will spend an average $142,000 on long-term care needs like nursing and help with daily activities like bathing and eating.

For women, the number reaches $176,000.

The figures come from a new report projecting the risk of needing long-term care. The U.S. Department of Health & Human Services commissioned the Urban Institute to create the report.1

The report finds that American men who turn 65 in 2020-2024 will require an average 2.3 years of long-term care.

Women can expect to need an average 3.2 years of long-term care.

Projected Need for Long-Term Care

U.S. Population Turning 65 in 2020-2024

But because Medicare doesn’t cover long-term care and Medicaid only does after people become impoverished, many aging Americans and their families can expect to foot the bill–or provide the care–themselves.

Rapidly Aging Population

The United States is experiencing sharp growth in the numbers of elderly people.

The 65 and over population is projected to expand from roughly 57 million today to over 80 million in 2050. Many of the elderly will be in the 85 plus bracket, the group that requires the most long-term care.

Only about 6% of Americans age 65-69 require services such as help bathing, eating, or other activities of daily living that meet the government’s disability** requirements for what it calls Long-Term Services and Supports (LTSS).

But by age 90, that figure grows to about half the population. People age 65 and up are projected to spend between 3-6 years in states of mild or severe disability, much of it at the end of their lives.

As a consequence of the expansion of this population, the number of people using long-term care will swell.

The report projects that in 2050 over 10 million Americans will require substantial assistance with at least two activities of daily life, or supervision due to severe cognitive impairment.

Who Will Pay

The topic of long-term care is poorly understood by the public. “People think Medicaid is delivering a lot of long-term care, but in fact the disableds’ families are,” notes the report’s author Melissa Favreault. “And we expect that to increase in the future.”

Medicaid currently covers about half of Americans’ long-term care, or about 0.4% of GDP. That figure is expected to stay about the same in coming decades, but the costs borne by families will rise dramatically.

The reality is that few Americans can afford pricy long-term care insurance, and a tremendous amount of care is being provided by spouses, children and siblings, uncompensated at home.

“It’s critical to save for long-term care,” says Favreault. “Some find the best way to do this is to buy private long-term care insurance, but there are a lot of challenges in this market.

“That said, for a lot of people saving is critical. You have a pretty good chance of facing expenditures in the hundreds of thousands of dollars, and for many middle and lower income families that level of savings is very difficult.”

Public Approaches to Long-Term Care

Much noticed among long-term care experts in President Joe Biden’s recent infrastructure plan was his proposal to spend $400 billion on home and community-based services, much of which would go toward helping Americans who require long-term care.

Some states aren’t waiting on the federal government to act but are instead implementing their own plans. The state of Washington recently passed the Washington Trust Act, under which residents pay a bit more payroll tax for a benefit to effectively cover the first year of long-term care.

“Part of the motivation is that now under current law Medicaid is the main public payer, but you have to impoverish yourself to qualify,” explains Favreault.

“Medicare doesn’t cover long-term care. There’s a sense we need to help people insure themselves better, and the private market is having trouble right now, so that’s why people have suggested we need more public long-term care insurance. People will pay a bit more tax when they’re young, so they’ll be eligible for care when they get older.”

With other states conducting feasibility studies on public long-term care insurance and holding referendums, more public policy solutions may be in the offing.

“Covid slowed the momentum, but the crisis underscored how vulnerable people in long-term settings can be,” Favreault observes.

“Once the economy stabilizes and the epidemic is under control, more states will be looking at this. I think it can provide a model.”

Resources

Reports on the current private long term care insurance market:

https://content.naic.org/sites/default/files/publication-ltc-lr-care-experience-report.pdf

Annual long-term care costs:

https://www.genworth.com/aging-and-you/finances/cost-of-care.html

Notes

* Projections are based on the Urban Institute’s tabulations from DYNASIM4, run id974. Published in PROJECTIONS OF RISK OF NEEDING LONG-TERM SERVICES AND SUPPORTS AT AGES 65 AND OLDER.

** “HIPAA level” disability is defined according to the Health Insurance Portability and Accountability Act as needing substantial assistance with at least 2 ADLs (Activities of Daily Life) or supervision due to severe cognitive impairment that is expected to last at least 90 days.